Shades of 1973 – 1974, The Grocery Aisle vs. The CPI, The Second Wave, & The Coming Fed Rate Hiking Cycle

Views From the Stream

Shades of 1973 – 1974, The Grocery Aisle vs.The CPI, The Second Wave, & The Coming Fed Rate Hiking Cycle

I remember the 1970s well. My parents worried about the cost of everything, which went up without end and much faster than their income. Just buying groceries was a big deal. Gasoline prices went through the roof. And there was rationing of when you could buy gasoline, with odd and even days depending on your license plate. I remember my parents sending me to wait on line to buy gas, hoping the gas station did not run out before it was my turn. (It was another wise decision by my parents, like buying cheap bananas for me to eat, as the wait was often 30 – 60 minutes or more as people lined up to fill their tanks.) Vacations consisted of driving to a motel by the shore and spending the time on the beach. No flights to somewhere far away and exciting. Not even to somewhere within the U.S. The price of gold soared to over $800 per ounce. I remember my Dad and Grandfather buying gold and silver. And then selling it at the end of the decade. And I remember how it all ended in the 1980 – 1982 Recession engineered by Paul Volcker to break the back of inflation. You could hear a pin drop in the malls, as they were empty.

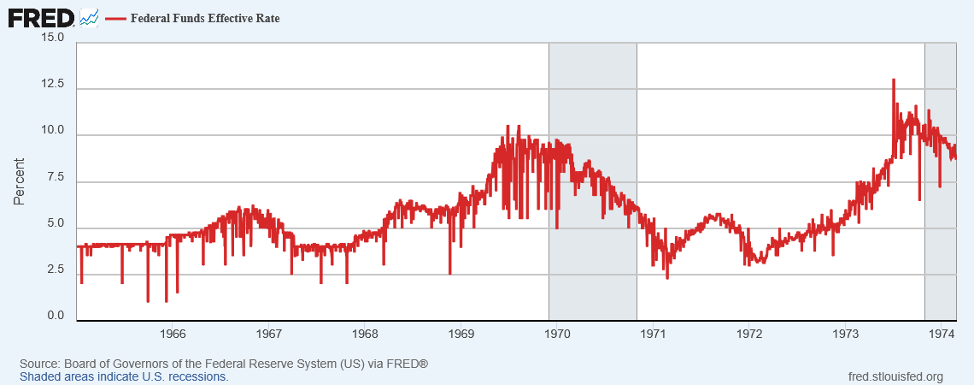

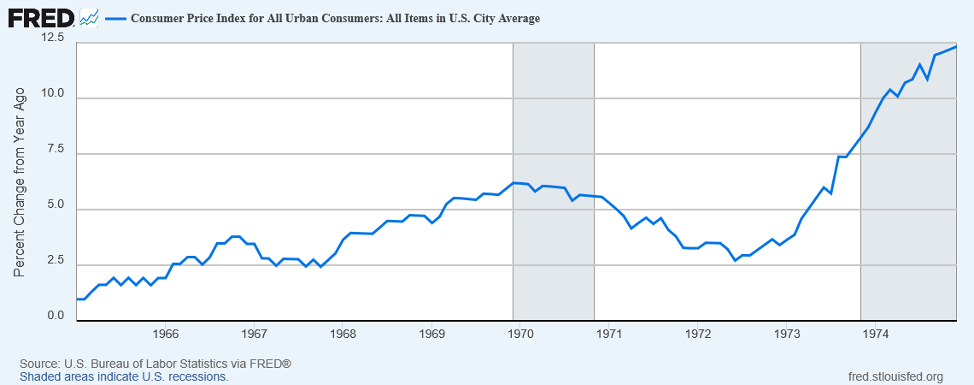

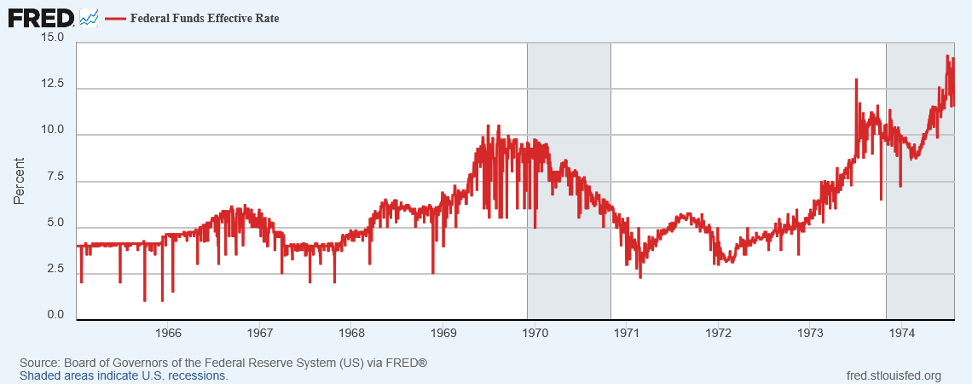

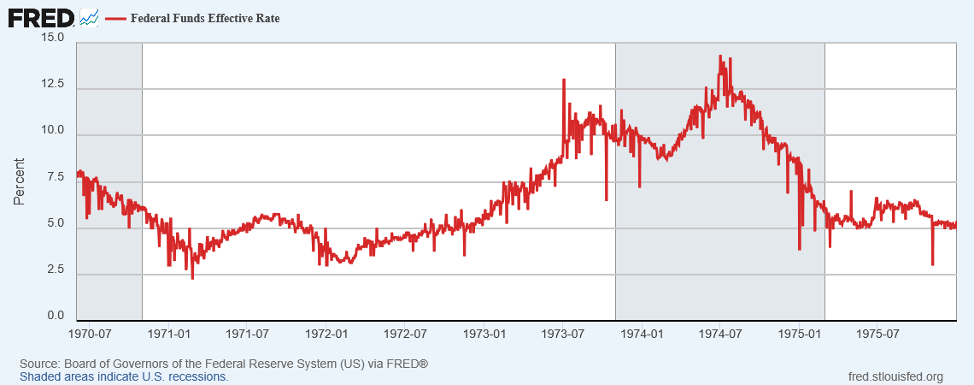

Today’s environment most closely resembles the 1973 – 1974 period. The Federal Reserve entered an easing cycle in early 1970 to combat the 1969 – 1970 Recession. This cycle ended in February 1971 as it became clear the economy was bottoming and turning up. However, Inflation reaccelerated with the economy. So, the Fed entered into a rate hiking cycle in March 1972, just a year after it finished cutting rates. This Rate Hike Cycle, which started with a 25 basis point hike to 4.00% in March of that year would not end until July 1973 at 11. 75%. The Fed, realizing another Recession loomed due to the huge rate increases, began to cut rates. This decision proved prescient as the economy entered Recession in November 1973. With Recession in the background and knowing Inflation lagged the economic cycle, the Federal Reserve continues to drop rates, which fell to 9.00% by February 1974.

However, the OAPEC Oil Embargo intervened. (At that time, OPEC was known as OAPEC, Organization of Arab Petroleum Exporting Countries. It subsequently dropped the A as the organization expanded beyond the Middle East.) In October 1973, in response to the Arab-Israeli Yom Kippur War, OAPEC announced a cut in production of 5% and an embargo of oil shipments to any country that supported Israel in the war. This initially meant the U.S., U.K., Canada, Japan, and The Netherlands. This led to oil prices rising 300% from $3 per barrel to $12 per barrel.

This oil shock flowed through everything in the U.S. economy from groceries to cement, as energy stood a major input into every good. Instead of decelerating with a lag, as the Federal Reserve expected due to the Recession, Inflation accelerated to above the Fed Funds rate.

In response, despite the Recession, the Federal Reserve had no choice but to raise rates to put some brakes on Inflation:

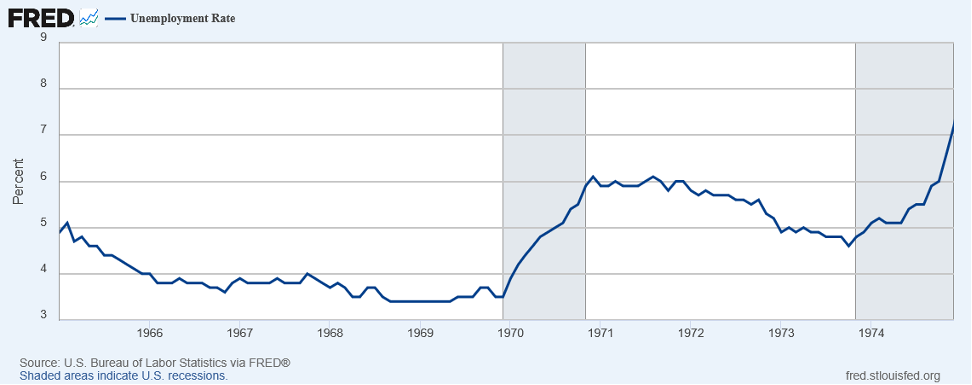

Fed Funds rose to almost 13.00% by July 1974. But, Unemployment, which had risen only marginally from 4.1% to 5.1%, began to explode upward.

The Federal Reserve came under intense political pressure to lower rates. And it did so:

The Federal Reserve only stopped lowering rates when the economy exited the Recession in March 1975.

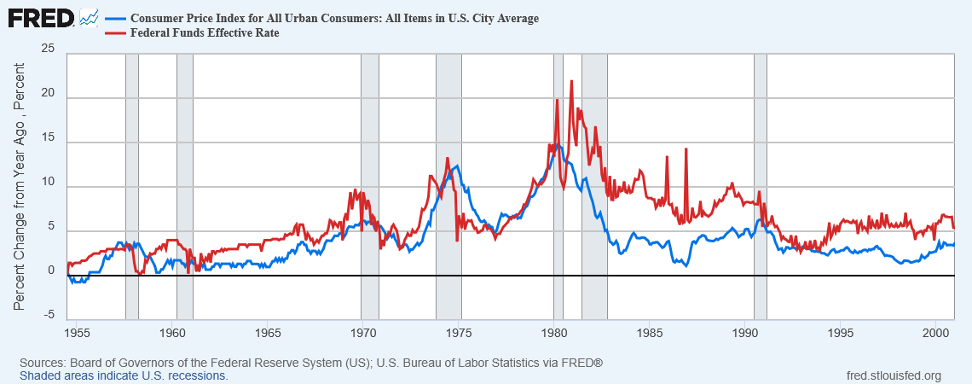

What one can note about the Federal Reserve policy that decade relates to the relationship between Fed Funds and Inflation. Fed Funds typically exceeded the Rate of Inflation during increasing Rate Cycles and then led Inflation on the downside during the 1960s and 1970s. Post 1980, Fed Funds remained well above the CPI to ensure Inflation did not return. That policy stayed in place until the early 2000s:

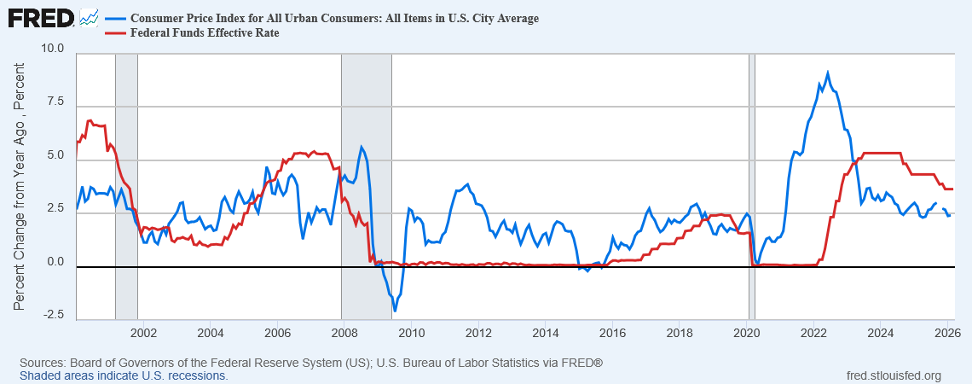

Starting in 2002, the Federal Reserve began to hold the Fed Funds Rate well below the rate of Inflation. This policy decision contrasted with the attempts to control Inflation put in place by prior Federal Reserve Chairmen since World War II. In fact, the Fed’s stated that it desired to raise the Rate of Inflation. Only in 2006 and 2007 did Interest Rates exceed Inflation when the Fed recognized the Housing Bubble and sought to address the excesses:

While it appears that the Federal Reserve returned to a policy of maintaining the Fed Funds above the Rate of Inflation, this appears an illusion. Prices in the Grocery Aisle continue to inflate between 5% and 10% on a year over year basis. For example, the price of chicken per pound just went up $0.50 per pound on a $6.00 base rate. That equates to an 8.3% price rise. The price of yogurt went from $4.99 on sale for 4 small containers to $5.39, 8.0%. Despite the removal of tariffs, the price of spaghetti on sale for the average family was up over 15%. The price of American Cheese and other similar products is up similar amounts. The price of tomato sauce is up over 9% year over year. The price of laundry products continue to rise as well. Over the past 18 months, the price of Hagen Daaz ice cream not on sale (a personal favorite) went from $8.99 to $10.99 for 28 fluid ounces, an increase of over 22%. (This excludes the reality that the container used to contain 32 fluid ounces, which Unilever shrank over the past five years in stages to the current levels.) These are basic staples (except for my favorite grocery store ice cream). Similar price increases can be found in the Big Box stores for items as diverse as paper towels, glass cleaner, and tuna fish. If one were to travel to other store types, clothing stores expect to raise prices 5% to 8% this year. As do many producers of goods to cover cost increases in their inputs. The latest PPI (Producer Price Index) rose 3.4% year over year as input costs began to accelerate. Local Governments continue to raise taxes on their citizens. Property taxes continue to rise on a national basis ahead of the CPI. For example, Minnesota plans to raise property taxes by 6.9%. This reflects local and state governments facing the same cost headwinds as consumers. NYC bridge and tunnel tolls rose 7.5%. Fares on the PATH train between NYC and NJ went from $3.00 to $3.25, an 8.3% increase. Fares will rise an additional $0.25 in 2027, 2028, and 2029. Even in a state like Texas, tolls are rising 3%. Based on this, consumers continue to view the reality of their register receipts over anything the government tells them. And this stands before the rise in energy prices due to the Iran War. With Inflation accelerating, the current history of the Fed Funds looks eerily similar to that from 1965 – 1973:

And with the damage to infrastructure in the Persian Gulf making clear that energy prices will not return any time soon to their pre-Iran War levels, Inflation appears set to accelerate just as in the 1973 – 1974 period. This coming Second Wave would mimic the history from the 1970s and other prior Inflation Cycles. (For more details, please see A 1970s Rerunpublished April 30, 2022.)

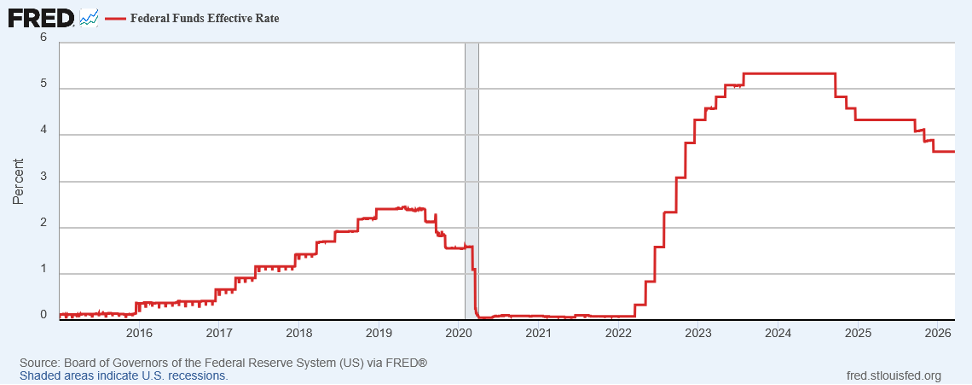

In his recent Press Conference that accompanied the official FOMC (Federal Open Market Committee) Release, Chairman Powell indicated the FOMC’s concerns about Inflation. Should Inflation reaccelerate, as seems likely, would Fed Rate Increases stand far behind? Highly Likely. And, given this, the markets began to discount this future reality. At the beginning of 2026, the futures markets expected 1 – 2 Fed Rate Cuts. Today, not only do markets not see Rate Cuts, they see the potential for Rate Increases. And with Inflation set to accelerate, it seems the Federal Reserve will have little choice but to repeat the history of 1973 – 1974 by raising rates against a slowing economy. Should this occur, turmoil in the financial markets could ensue given the valuations of equities, the looming issues in private credit, the affordability issues in Housing, and the continued squeeze on consumer wallets.

With Shades of 1973 – 1974 looming over the economy, the average consumer appears set to relive the experience of my childhood. And given the Grocery Aisle vs. The CPI, consumers continue to believe their “lying eyes”. Given the Iran War and damage to infrastructure, a Second Wave appears inevitable. And with The Coming Fed Rate Hike Cycle set to hit the economy, a potential Recession lies in wait. For Consumers, its time to batten down the hatches as the brewing storm on the horizon rushes towards the U.S. economy.

Recent & Upcoming Travel

Travel lately consisted of numerous trips to New York City. Despite a socialist Mayor, the city appears thriving as the subways, sidewalks, and restaurants appear packed with people. While I managed to travel there on some beautiful springlike days in early March, my view consisted of the inside of a conference room and an elevator bank. However, the networking with other family offices more than made up for the lack of view.

As to fishing, the fly fishing season officially opens April 1. However tempted I am, I know better than to show up on Opening Day as the streams tend to be quite crowded. But I do plan to buy my fishing license and show up over the next few weeks to test the Spring fishing.

Pickleball and Latin Dancing continue to occupy my free time. Both are quite social and I have had the opportunity to meet many fascinating and wonderful people from all walks of life. It reminds me of martial arts which attracted everyone from a person who drove a truck to a partner in a private equity firm. These new pursuits keep me in touch with people from all over and remind me of how similar we all are.

And with spring busting out all over, I have tended to my indoor garden. It began to bloom recently and I have numerous plants on the way to bloom, such as an orchid I received as a gift. Despite my lack of knowledge, it appears that the orchid will bloom again just 8 months after I received it in bloom. I feel blessed to have these plants share my daily life.

With that, we will report back next time on our future travels, new hobbies, and fishing tales, providing color on the happenings in the U.S. and around the globe.

Yours Truly,

Paul L. Sloate

Chief Executive Officer