Housing: The Laws Of Economics Win

Views From the Stream

Housing: The Laws Of Economics Win

In the early 1990s, I remember shopping for my first house. I was working on Wall Street and my former wife was a doctor. So, we were earning a good living. Despite this, given how expensive rentals were in NYC and the cost of living there combined with repaying my student loans, we scrimped and saved for the down payment for a house. Given Mortgage Rates of 9.5% – 10.0% at the time, we searched and searched for something we could afford. Eventually, we found a tiny house in Larchmont, NY for which we could make the numbers work. And we bought it.

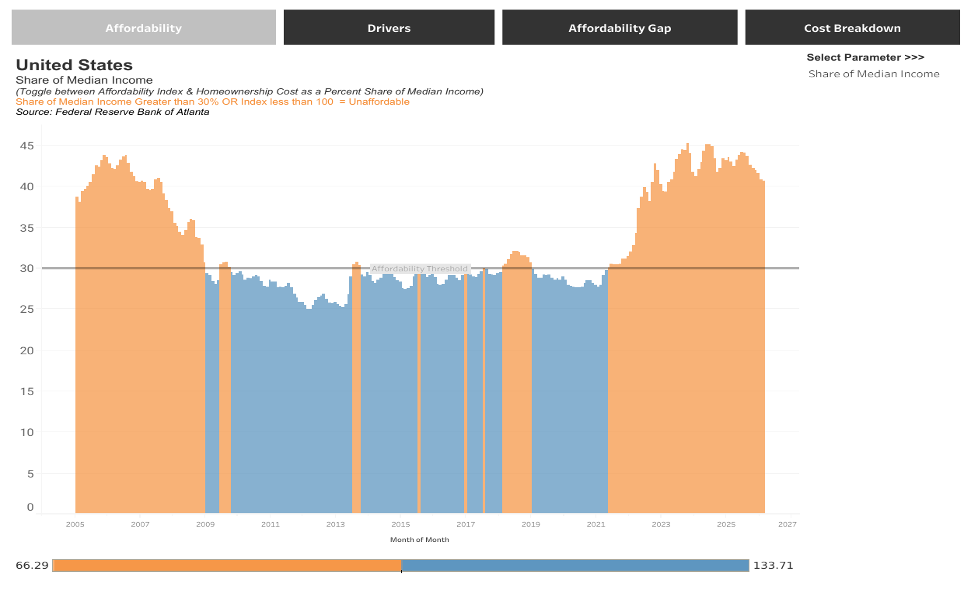

Today’s environment reminds me of that time. The cost of a home stands high relative to income:

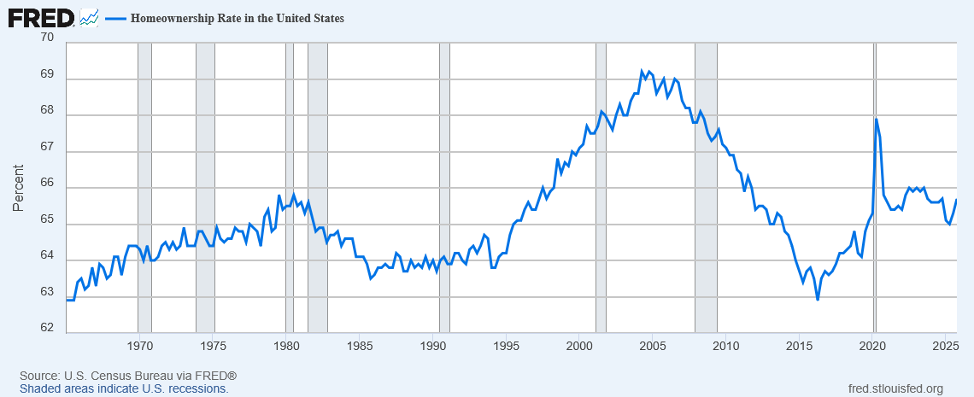

At 41% of Median Income, this ratio stood higher only from July 2005 to September 2006 or during the late 1980s. Despite this, Home Ownership stands at the upper end of long term averages, excluding the Housing Bubble:

At 41% of Median Income, this ratio stood higher only from July 2005 to September 2006 or during the late 1980s. Despite this, Home Ownership stands at the upper end of long term averages, excluding the Housing Bubble:

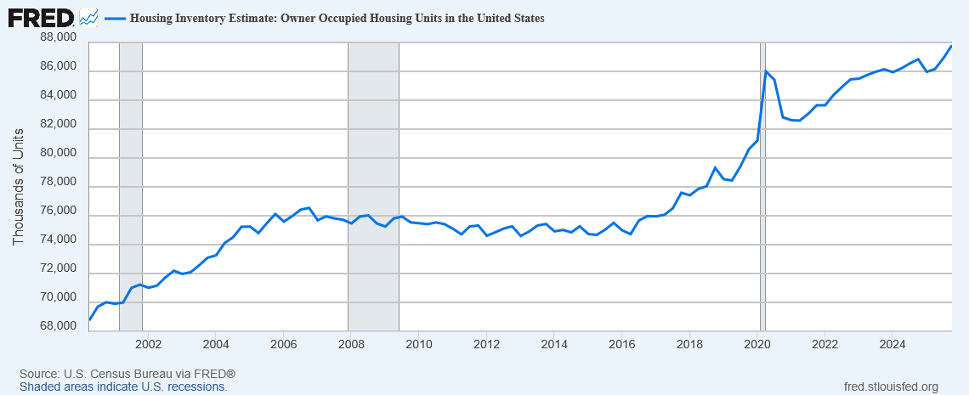

In addition to the recovery in Home Ownership back to strong levels, the number of Home Owners, as measured by Households, continues to grow at a steady pace, rising from ~74.5 million in 2016 to almost 88 million today:

This data suggests there exist sufficient units to absorb the growing ranks of those aspiring to Home Ownership.

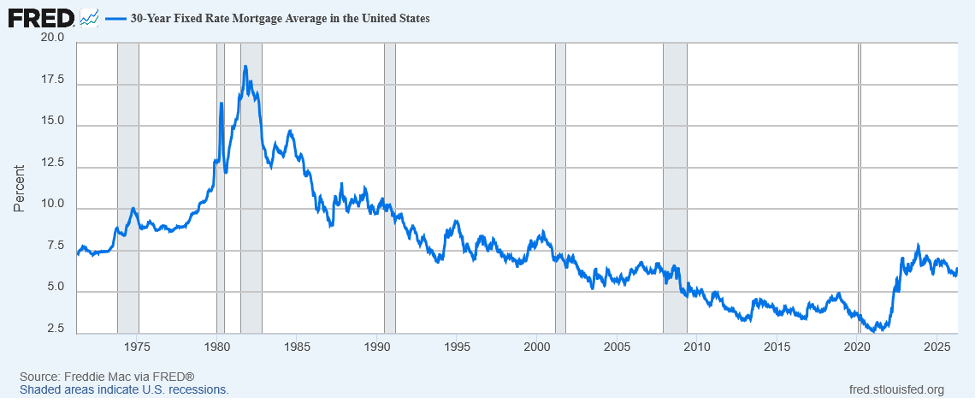

Despite this, the media and Congress continue to discuss a Housing Shortage. What they mean is Housing Affordability, as measured by the Atlanta Fed above, and current Mortgage Rates:

While Mortgage Rates did rise significantly over a short period of time from abnormally low levels in the 2019 – 2022 period, they merely returned to their pre-2008 levels and stand below the levels of the 1990s and 1980s. Thus, they do not appear abnormally high. And a few years of Home Prices moving sideways should cure any affordability issues as incomes catch up with Mortgage Rates.

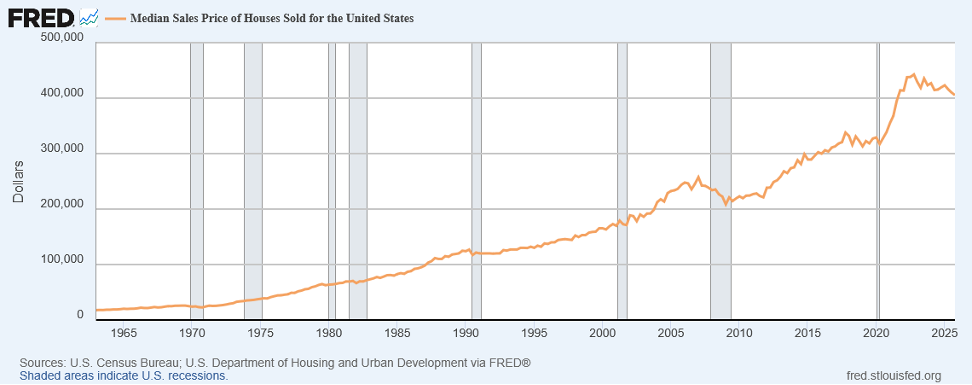

Affordability usually is a combination of prices and mortgage rates. Of course there are exceptions. In places like Florida, where hurricanes can have an outsized impact on insurance costs, insurance costs can impact affordability significantly. For most Americans, however, Price and Mortgage Rates dominate. And Price began to adjust to the reality of incomes over the past few years:

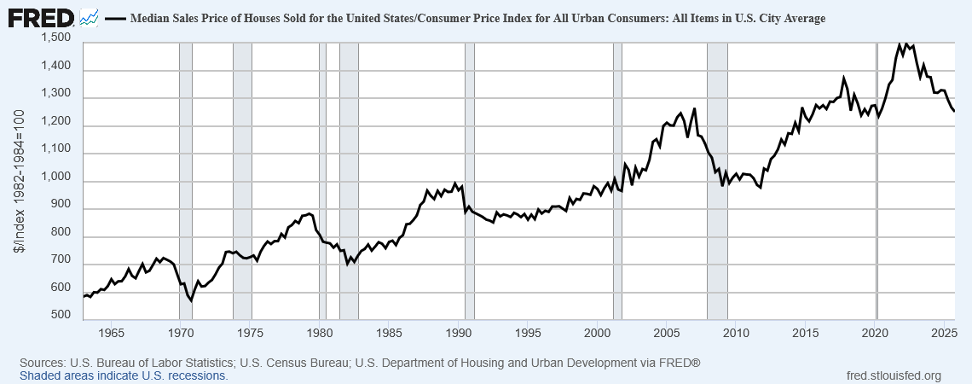

And, when Median Home Sales Prices are adjusted for Inflation, Real Sales Prices have returned to their pre-Pandemic levels:

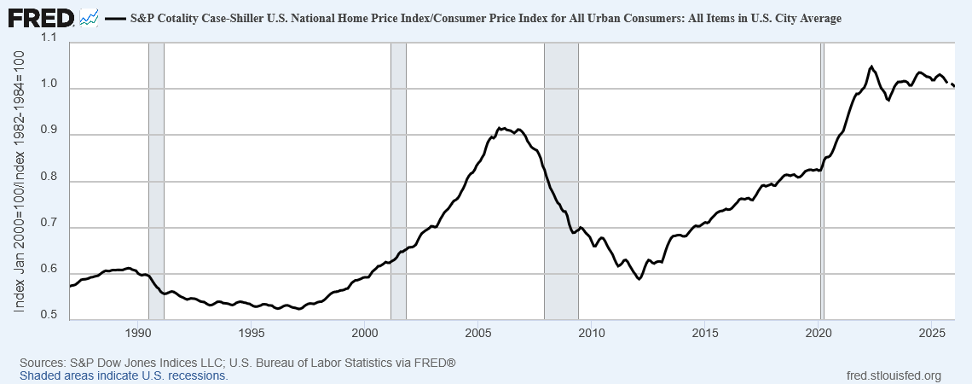

Even the Case Shiller Index indicates Real Home Price Sales have flattened out over the past several years:

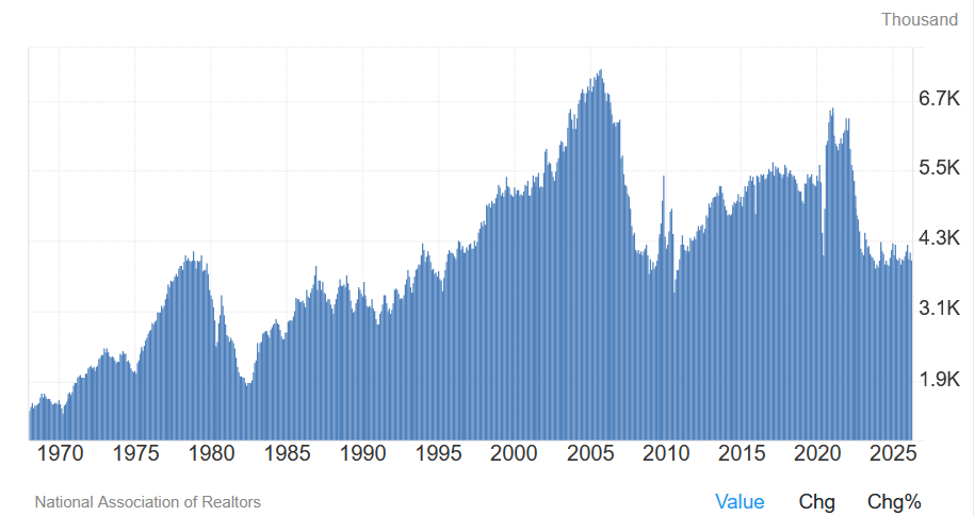

Thus, the Housing Market continues to adjust to the underlying economic reality. However, given the spike in Mortgage Rates, Existing Home Sales, after approaching levels last seen during the Housing Bubble, collapsed to post Bubble lows:

And they continue to run along at low rates. With incomes continuing to grow and housing prices flat, Affordability should improve over the next few years, driving Existing Home Turnover upward, with a lag. Interestingly, Data from Public Homebuilders indicates Unit Sales remain at high levels despite the rise in prices and interest rates. For most homebuilders, recently reported orders either remain flat or continue to grow. Some homebuilders reported strong orders, such as DR Horton whose orders rose 11% year over year for its new homes. This does not indicate a fundamental problem in the Housing Markets, but time needed for incomes to catch up with housing costs.

For young renters aspiring to buy homes, the Housing Market may appear expensive. But, as when I bought my first home, savings plus cutting back on other expenses should enable a new generation to buy despite low Home Affordability. Home Ownership rates stand consistent with this. And it appears the Housing Market continues to adjust to the reality of higher Mortgage Rates and the changing fundamental backdrop. With data indicating continued steady growth in Households Owning A Home, it appears The Laws of Economics continue to dominate.

Inflation: The Second Wave

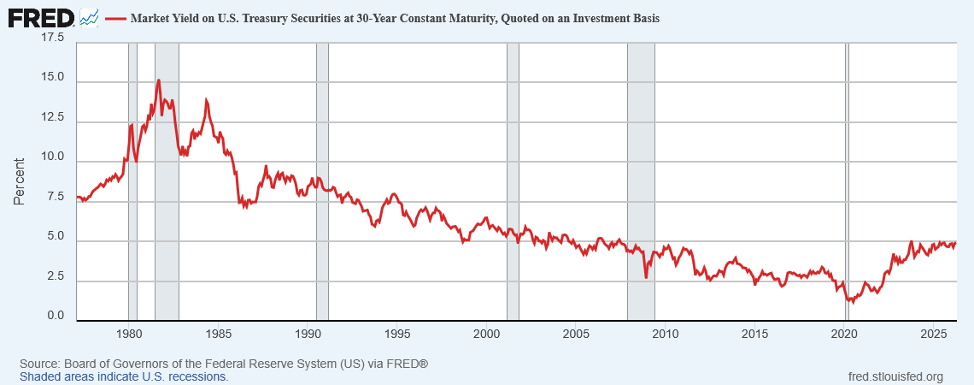

For those of us who live in the real world, it appears that Inflation began to accelerate in Q1 and will continue to do so as the year progresses. Companies raised prices in Q1, even before the turmoil in the Gulf, and plan to raise them more in Q2. For example, Fastenal, an industrial distribution company, realized price increases of 3.5% in Q1. PPG, a major global paint and coating manufacturer, announced price increases in April of up to 20% on its products due to the rising cost of inputs. Major consumer companies began to raise prices in Q1 as well, which will continue in Q2. For example, the price of Dove Soap Bars, made by Unilever, just went up 7.7%. The “on sale” price of Tide Detergent, manufactured by P&G, rose 6.25%. Other consumer product companies plan to follow. In addition, rising transportation costs will lead to further price pressures. Major trucking companies already announced fuel surcharges. And airlines continue to raise prices to “recover” their rising jet fuel costs. While the Federal Reserve states it will “look through” these price increases as “Transitory”, the Bond Market may not be so forgiving. The First Inflation Wave occurred from early 2021 to mid 2023. This occurred less than 3 Years ago. Despite falling back from peak levels, the Monthly CPI fluctuated between 2.4% and 3.3% year-over-year over the past two years. This works out to a 2.8% – 2.9% median level. And with Inflation poised to accelerate, the 30 Year Treasury Bond continues to press up against 5%, threatening to break through to higher yields:

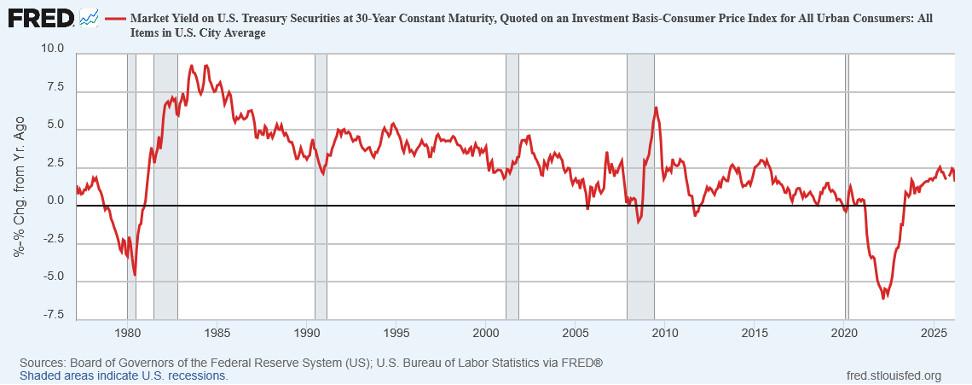

With the March CPI at 3.3% and headed higher, such a move stands reasonable. Unlike the 3 Month Treasury Bill, whose rates are linked to Federal Reserve policy, the 30 Year Treasury Bond’s yield stands determined by market forces. And historically, yields exceed the rate of inflation:

With a minimum 2.5% yield premium to Inflation in periods of higher Inflation and Inflation, as reported in the CPI, averaging more than 4.5% since March 2021 and over 3% for the period since May 2023, post the Inflation spike, it seems reasonable that 30 Year Treasuries should yield 5.5% or more. This would merely return Yields back to levels of the 1990s, when Inflation averaged 3%+.

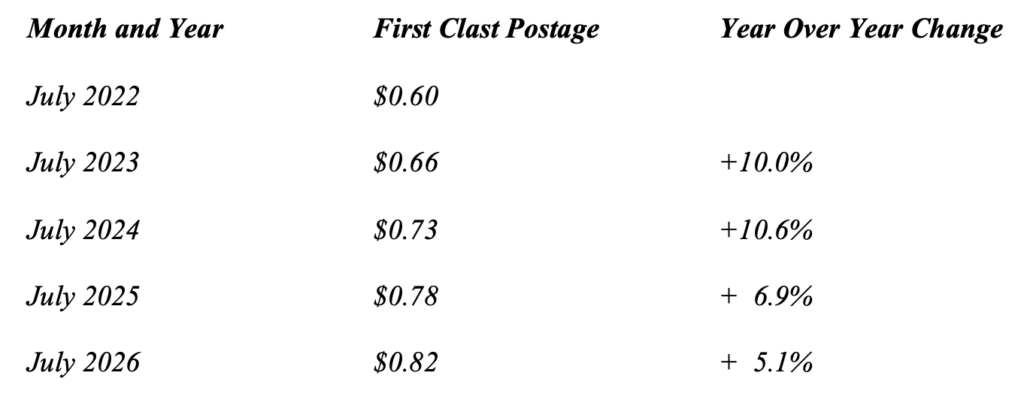

We note that these Inflation statistics, as published by the Government, appear to understate real world Inflation for the Consumer, even as imparted by the U.S. Government itself. The price of a First Class Postage Stamp represents a cost that touches everyone:

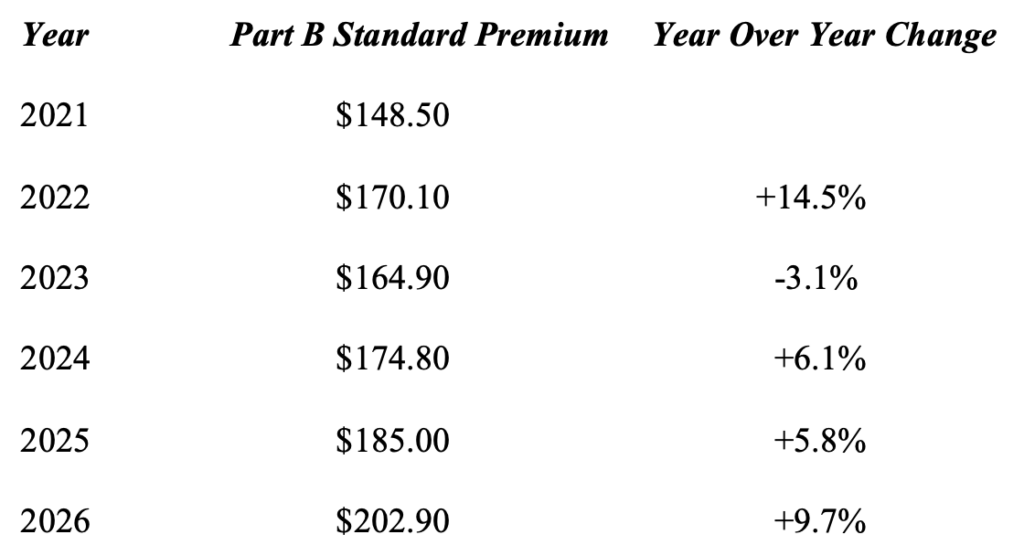

This works out to an 8.1% compound increase over the past four years to mail a letter. And this excludes the 8% fuel surcharge the U.S. Postal Service imposed starting April 26, 2026. Separately, one can examine Medicare premium increases for retirees over the past 5 years:

For seniors, a 6.4% compound increase over the past five years stands well above the growth in their Social Security payments. Should these statistics represent something closer to the truth about inflation, then 30 Year Treasuries could Yield considerably more than the 5.5% noted above. Welcome to The Second Wave.

Private Credit: More Cockroaches

Two more cockroaches emerged recently in the Private Credit arena. They are large loans to two software companies owned by private equity firms: Medallia and Qualtrics. In December, Blackstone and KKR wrote their Medallia loans down to $0.80 on the dollar lent. Over the past week, they wrote the loan down to $0.60 on the dollar lent. These latest losses will only bring more questions on Private Credit marks, especially those related to private equity loans. The potential losses prompted UBS this past month to issue a report indicating Private Credit losses could double this year to 9% – 10% of the underlying assets. And this stands before any recession. As the cockroaches continue to emerge, there exists growing risk that the damage will spread beyond Private Credit to broader sectors of the financial markets, including banks and insurance companies. And then ultimately to the economy at large. The snowball appears rolling down the mountain. And only time will tell if it becomes an avalanche.

The China Export Relief Valve: Begger Thy Neighbor At Work

China continues to utilize Exports to offset Falling Domestic Demand. Autos stand a clear example that one can replicate across numerous sectors of the Chinese economy. In Q1 2026, China’s Domestic Demand for Autos fell ~300,000 units year over year. To avoid a contraction in auto manufacturing and the obvious negative impact across large facets of its domestic economy, Chinese Unit Auto Exports magically rose ~300,000 units in Q1, offsetting 100% of the fall in Domestic Demand. While good for China’s manufacturers and economy, as production remained stable, this stands bad for the rest of the world as Chinese Exports displaced other countries’ domestic production. With this Begger Thy Neighbor Policy, China continues to export its economic troubles away. With the rest of the world beginning to say No, expect Global Trade to continue to come under assault as foreign markets close to Chinese goods and the country faces the consequences of its massive overcapacity.

Recent & Upcoming Travel

A quick trip to Miami this month reminded me of the boom bust nature of Florida. Construction Cranes dominated the landscape in the city’s financial district. And after a poor 2025 for the state’s housing market, excluding the ultra-luxury segment, sales appear on track to return to 2023/2024 levels. According to Redfin, single family home sales rose 7.7% year over year in March, consistent with those years. And given the continued in migration, Florida housing should continue resilient.

As to fishing, the fly fishing season officially opened April 1. Unfortunately, between travel, running two companies, and my new hobbies, my rods continue to gather dust. I do now have a date on the calendar to remedy this. So, next month, I hopefully can share my fish tales once more.

Pickleball continues much fun. After almost two years, I finally have begun to see the court and plan out my shots. And this certainly has impacted my game, as my win percentage continues to creep upward. With Spring arriving, Latin Dancing moved into a new phase, outdoor dancing. With the weather turning benign, numerous social dance events take advantage of the warmer weather. And hundreds of local dancers converge at these events to enjoy the great outdoors.

My indoor garden continues to reward me with bloom. My amaryllis continue to bloom in sequence. And evidently despite violating “proper” Orchid care, my Orchid appears not to have noticed. According to the experts, I should cut the flower spike back when the plant finishes blooming. I guess I don’t listen well. Since no one exists in the wild to cut these spikes back, I decided to let the plant tell me about the flower spike. It remained green and healthy, appearing happy. So, I left it alone. And then it threw out a flower spike recently. This first spike appears set to provide four blooms. And yes, the word “first” is not an accident. The Orchid appears set to throw a second flower spike. Time will tell. But Nature stands amazing and always surprising.

With that, we will report back next time on our future travels, new hobbies, and fishing tales, providing color on the happenings in the U.S. and around the globe.

Yours Truly,

Paul L. Sloate

Chief Executive Officer