The Carrot & The Stick Part II: The Ascendance of the National Interest

psloate

Click to download our newsletter in its entirety

“The growth of cities has gone on beyond comparison faster than the growth of the country, and the upbuilding of the great industrial centers has meant a startling increase, not merely in the aggregate of wealth, but in the number of very large individual, and especially of very large corporate, fortunes. The creation of these great corporate fortunes has not been due to the tariff nor to any other governmental action, but to natural causes in the business world, operating in other countries as they operate in our own.

The Process has aroused much antagonism, a great part of which is wholly without warrant. It is not true that as the rich have grown richer the poor have grown poorer. On the contrary, never before has the average man, the wage-worker, the farmer, the small trader, been so well off as in this country and at the present time. There have been abuses connected with the accumulation of wealth; yet it remains true that a fortune accumulated in legitimate business can be accumulated by the person specially benefitted only on condition of conferring immense incidental benefits upon others. Successful enterprise, of the type which benefits all mankind, can only exist if the conditions are such as to offer great prizes as the rewards of success. … All this is true; and yet it is also true that there are real and grave evils, one of the chief being over-capitalization because of its many baleful consequences; and a resolute and practical effort must be made to correct these evils.

There is widespread conviction in the minds of the American people that the great corporations known as trusts are in certain of their features and tendencies hurtful to the general welfare. This springs from no spirit of envy or uncharitableness, nor lack of pride in the great industrial achievements that have placed this country at the head of the nations struggling for commercial supremacy. It does not rest upon a lack of intelligent appreciation of the necessity of meeting changing and changed conditions of trade with new methods, nor upon ignorance of the fact that combination of capital in the effort to accomplish great things is necessary when the world’s progress demands that great things be done. It is based upon sincere conviction that combination and concentration should be, not prohibited, but supervised and within reasonable limits controlled; and in my judgment this conviction is right.”

First Annual Message to Congress President Theodore Roosevelt December 3, 1901

With the end of the Cold War, coupled with a decision the country could loosen import and export controls in place for the past 50 years to win the Cold War, the government loosened the rules to allow more free trade. The thought process behind these actions assumed US exports of high value goods would soar as other countries loosened import barriers. Thus, Congress approved both NAFTA and the WTO. The reality turned out quite differently. As Ross Perot predicted during the Second Presidential Debate in 1992:

“It’s pretty simple: If you’re paying $12, $13, $14 an hour for factory workers and you can move your factory South of the border, pay a dollar an hour for labor,… have no health care – that’s the most expensive single element in making a car – have no environmental controls, no pollution controls, and no retirement, and you don’t care about anything but making money, there will be a giant sucking sound going South.”

One would say a no brainer, given Ross Perot’s analysis. On top of this analysis, other countries encouraged the movement of manufacturing to their domestic markets by providing incentives and tax breaks. They then took advantage of US rules to export goods back to the US and lowered the value of their currencies to ensure their exports stayed low cost as their labor rates rose. For corporations, this leveraging of “Free Trade” enabled them to lower their costs while maintaining prices in their core markets. In addition to a set of trade rules tailor made for this type of action, as it exempted many of the emerging market countries from the rules of engagement imposed on developed countries like the US, corporations benefitted from the lowering of US effective corporate tax rates, from over 30% in 1990 to under 20% today. This enabled companies both to keep a larger portion of their corporate income and to take advantage of lower foreign labor costs by locating manufacturing outside the United States. In addition, with the US moving to not tax profits left abroad, the government created further incentives to move operations outside the US and to create profits in low tax jurisdictions. Lastly, with the move to a more conservative judiciary as well as Congressional legislation removing state consumer protections in favor of national legislation, corporations benefitted from a legal climate tilted in their favor.

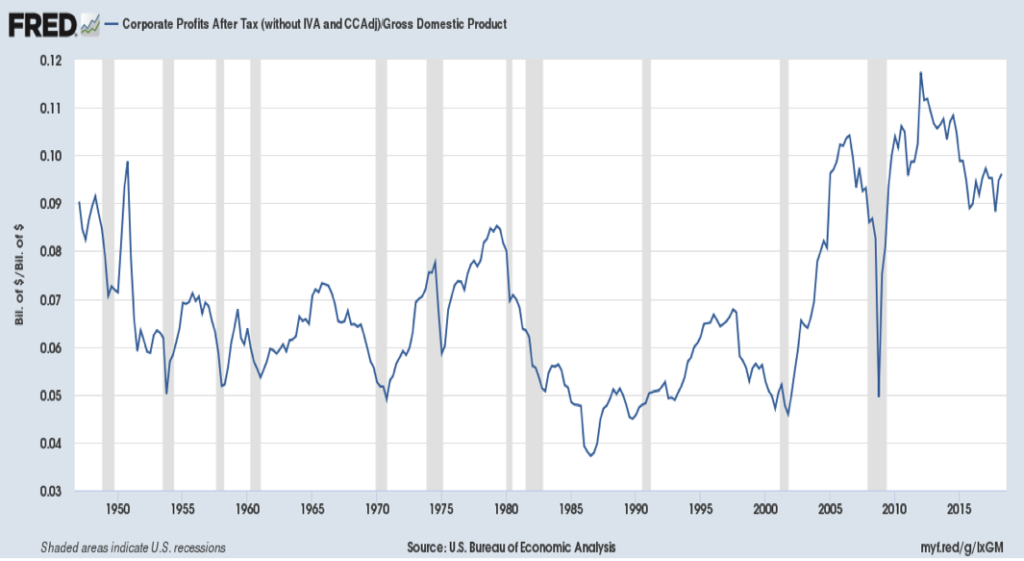

For large corporations, just about everything went right over the past 25 years. Combined, these actions significantly enhanced corporate share of US GDP, as the following chart demonstrates:

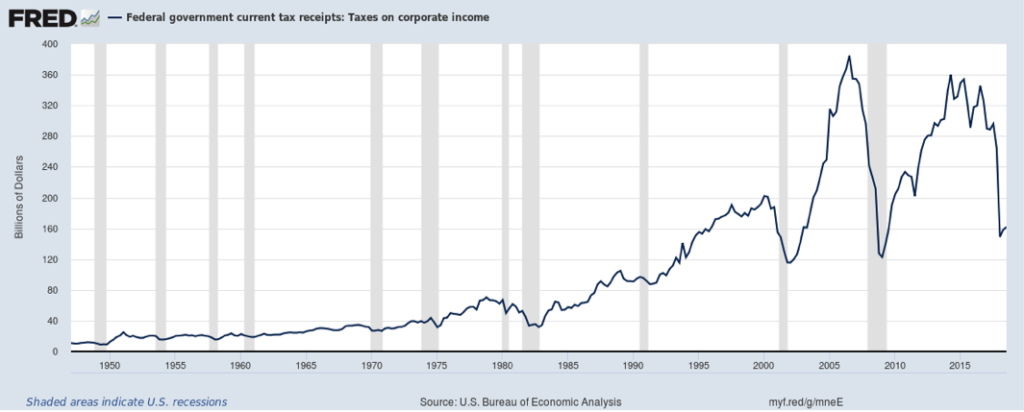

These actions, however, led to a perverse outcome for the United States. While corporate profits continued to grow, companies’ tax contribution to support the government and government institutions that protected their assets at home and abroad stagnated for the past 20 years and fell 45% in real terms. The following chart shows that corporate tax receipts today stand somewhere near their 1996 level despite more than a doubling in the size of the economy since then:

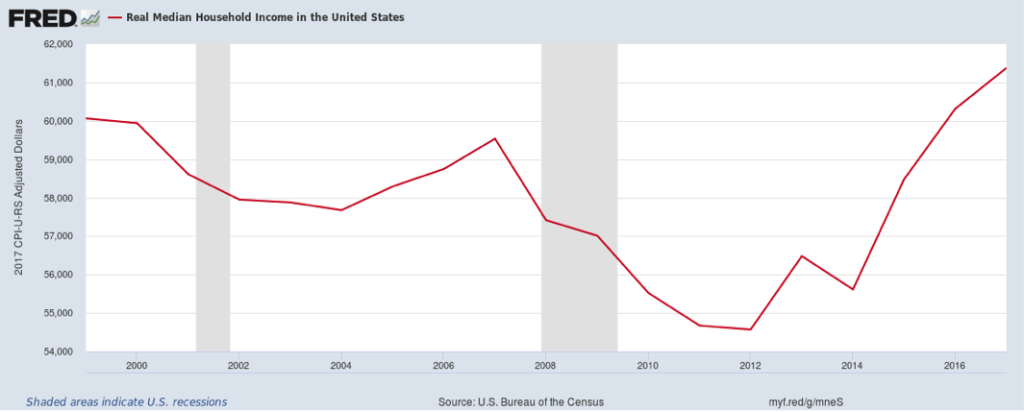

As would also seem obvious, as factory jobs moved abroad, overall Labor Income stopped growing and the tax burden rose for the average family. As the following chart demonstrates, Real Median Household Income stands less than 2% above its level in 1999:

Furthermore, the country’s industrial base eroded as Manufacturing Investment to GDP collapsed. This investment went abroad instead, as companies established manufacturing bases to access Emerging Economies and built excess capacity to export back to the US. And lastly, corporations moved to put other countries interests ahead of that of the United States. One need only look at Google’s refusal to help the US government in Artificial Intelligence but willingness to comply with Chinese rules or Boeing’s planned sale of advanced satellite technology to China despite US export rules forbidding it. (Boeing magically cancelled this sale when the Wall Street Journal ran a front page article outlining how Boeing deliberately ignored government rules in order to make a satellite sale.) As one might say, not the intended result.

While some of these trade moves initially made sense to encourage corporate investment and to potentially increase the amount of exports from the United States to foreign countries, the execution by Corporate America leaves much to be desired. And recent actions appear at odds with the old adage: “Don’t bite the hand that feeds you.” With a dormant global strategic rivalry with China heating up, once again, and a likely return to the Cold War mentality that ruled the 1950s and 1960s, the world will become a very different place for corporations that have ruled the roost over the past 25 years. These changes will come in stages as the United States acts to put its interests first, in order to meet the global challenges of today while providing its citizens a higher standard of living over the long term.

The first and most obvious change will come under the rubric “National Defense”. While the term National Defense clearly covers jet fighters, tanks, and naval ships, it more broadly covers the country’s ability to wage war and to maintain a strategic advantage over other rival countries. In simplest terms, it means maintaining a military of sufficient size to protect the country and to reach overseas as needed. If it is not there when you need it, you have a big problem. As Teddy Roosevelt clearly stated in his 1901 Annual Message to Congress:

“It is not possible to improvise a navy after war breaks out. The ships must be built and the men trained long in advance. Some auxiliary vessels can be turned into makeshifts which will do in default of any better for the minor work, and a proportion of raw men can be mixed with the highly trained, their shortcomings being made good by the skill of their fellows; but the efficient fighting force of the Navy when pitted against an equal opponent will be found almost exclusively in the war ships that have been regularly built and in the officers and men who through years of faithful performance of seas duty have been trained to handle their formidable but complex and delicate weapons with the highest efficiency. In the late war with Spain the ships that dealt the decisive blows at Manila and Santiago had been launched from two to fourteen years, and they were able to do as they did because the men in the conning towers, the gun turrets, and the engine-rooms had through long years of practice at sea learned how to do their duty.”

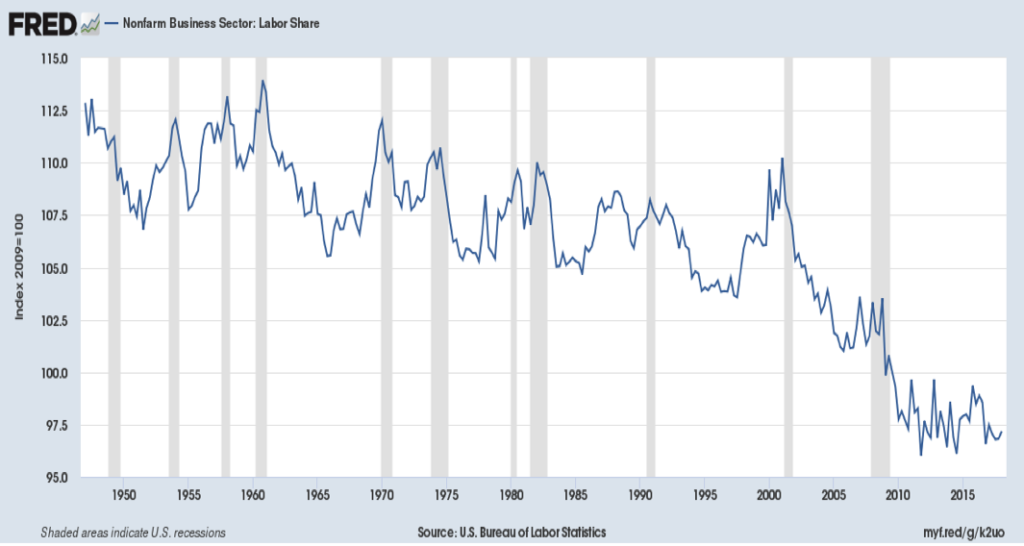

At the same time, companies will experience reverse labor arbitrage. In other words, they will hire more expensive labor in the US to replace less expensive labor in places like Malaysia, Indonesia, The Philippines, India, … Thus, the Corporate Profit Share of GDP will fall. For politicians, this will have the added benefit of improving real incomes in the US and increasing workers share of GDP, undoing the past 20 years fall:

But National Defense means much more than just having the armaments available. It means maintaining a technological edge against your opponent and ensuring viable supply lines in times of war. In other words, once National Defense comes into the equation, locating a key plant overseas that might not be accessible in time of war becomes problematic. In fact, it dictates that such goods must be manufactured in the home country. In other words, there must exist a National Security Industrial Base. For Manufacturing and Technology Companies that spent the better part of the past 20 years locating plant overseas to drive profit margins, this lens applied to their actions will come as a shock to the system. The government might simply state: “In the name of National Defense, manufacture of the following item will occur in the Continental United States.” Furthermore, the government likely will state that advanced technology and manufacturing, such as artificial intelligence, advanced semiconductors, additive manufacturing, and robotics, cannot be licensed to certain countries nor exported to plants in foreign countries except with prior approval of CFIUS. For companies that have grown used to acting to maximize corporate profits above all else by locating plant across the world or selling product to anyone, as corporate management sees fit, life will become very difficult. Overseas markets will become more limited and investment will rise.

For labor, National Defense would indeed be a boon as Real Incomes grew at or above GDP growth. For corporations, a potential profit squeeze lies ahead. However, given that corporate profit margins stand at levels last seen in the 1920s or in the post – WW II economic boom, this would merely represent a reversion to the norm.

To offset this labor cost pressure, companies will invest in capital in order to increase productivity. For the country, this will come as a positive, as volume growth and investment in new plant and equipment will accelerate economic growth. However, for company managements, the balance of cash thrown off of the business will shift from “Shareholder Return” to “Capital Investment”. For example, for the S&P 500, Shareholder Return projections for 2019 equal $1,300 billion compared to just $700 – $750 billion for maintenance and growth capital. Should companies return to the 60/40 split towards capital investment that existed during the 1990s, then capital investment could rise to $1,200 billion or more while Shareholder Return could fall to $800 billion or less. For companies driving earnings growth through share buyback and using corporate cash to offset stock option issuance, the true dilutive impact of those stock options would shine forth as buybacks collapsed. For the S&P 500, of the 5.4% compound growth in reported Earnings Per Share from 2007 to 2018, ~2% came from share buybacks. Fundamental earnings growth without shrinkage of the share base totaled less than 3.5%. Yet, corporate managements were handsomely rewarded as they shrunk their invested capital. In addition, Corporate R&D to Revenue likely would rise, as companies no longer could outsource this R&D to foreign labs or R&D centers set up in foreign countries. Adding to this issue, to put in place new machinery, more money would end up in Development to optimize all the new capital placed in service. These dollars would put additional pressure on operating margins. And while Corporations were offered the Carrot of low tax repatriation to bring cash back for investment, statistics demonstrate corporate use of this cash for more buybacks.

Unbeknownst to the average shareholder, much of the rise in corporate margins relates to the massive fall in depreciation as corporations invested less and bought back gobs of stock to drive Return on Capital upward at the same time as they shrank their share base. Actual EBITDA margins today of 17% to 18% look no different than from 1995 to 2000. Yet, Operating Margins soared over the past 20 years. Should Capital Investment return to prior norms, Operating Margins would fall 25% if they just returned to 2007 levels and between 40% and 50% were they to retrace all the way to 1998 levels. Coupled with a larger invested capital base and limits on share buybacks, Return on Invested Capital would shrink back towards normalized 1990s levels.

For those thinking this scenario stands as a fringe outcome, unlikely to occur, a quick read through the Executive Summary of The Assessment and Recommendations of the National Defense Strategy Commission would disarm such notions. (The document can be found at: https://www.usip.org/sites/default/files/2018-11/providing-for-the-common-defense.pdf.) The document clearly tees up such issues for a clean shot straight down the fairway. As it states on Pages viii and ix:

“Aggressively pursuing technological innovation and introducing those advances into the force promptly will be critical to overcoming operational challenges and positioning the U.S. military for success. We remain concerned, however, that America’s edge is diminishing or has disappeared in many key technologies that underpin U.S. military superiority, and that current efforts to offset that decline are insufficient … DOD and the U.S. government more broadly must take additional steps to protect and strengthen the U.S. National Security Innovation Base, perhaps by increasing investment in key industries and pursuing selective economic disintegration with rivals to avoid dangerous dependencies. The Department must also continue broadening its efforts to find and incorporate new capabilities commercially developed by the private sector. Not least, Congress and DOD must find new ways of enabling more rapid maturation, acquisition, and fielding of lead-ahead technologies.”

“A solid defense industrial base is a national priority, including an innovative and profitable domestic manufacturing sector with resilient supply chains. America’s manufacturing and defense industrial base and supply chain is essential to economic prosperity and national security. This industrial base must continuously innovate in order to remain economically competitive and to provide America’s warfighters with the capabilities to prevail in any conflict.”

For companies, the future will look much less like the past 25 years than the 40 years before then. During that time, the US fought numerous proxy wars against its strategic rivals and the lens of National Defense and National Interest dominated decisions. No investment overseas came without clear vetting by the government to allow both technology and capital to move abroad outside of our long term allies. For corporations, the Stick of the National Interest will move into Ascendance as the words Teddy Roosevelt spoke to Congress in 1901 reverberate through the halls of history:

“While awarding the fullest honor to the men who actually commanded and manned the ships which destroyed the Spanish sea forces in the Philippines and in Cuba, we must not forget that an equal meed of praise belongs to those without whom neither blow could have been struck. The Congressmen who voted years in advance the money to lay down the ships, to build the guns, to buy the armor-plate; the Department officials and the business men and wage-workers who furnished what the Congress had authorized; the Secretaries of the Navy who asked for and expended the appropriations; and finally the officers who, in fair weather and foul, on actual sea servic3e, trained and disciplined the crews of the ships when there was no war in sight – all are entitled to a full share in the glory of Manila and Santiago, and the respect accorded by every true American to those who wrought such signal triumph for our country. It was forethought and preparation which secured us the overwhelming triumph of 1898. If we fail to show forethought and preparation now, there may come a time when disaster will befall us instead of triumph; and should this time come, the fault will rest primarily, not upon those whom the accident of events put in supreme command at the moment, but upon those who have failed to prepare in advance.”

And with The Ascendance of The National Interest, a world thought far removed from today will return with a vengeance, upending current assumptions and setting the country upon a new course requiring corporations to once more put the United States interests ahead of their own. (Data from public sources coupled with Green Drake Advisors analysis.)