Revenge of the Supermarkets

“The entry into an industry (by either acquisition or internal development) of an established firm is often a major driving force for industry structural change. Established firms from other markets generally have skills or resources that can be applied to change competition in the new industry; in fact this often provides a major motivation for their entry decision. Such skills and resources are very often different from those of existing firms, and their application in many cases changes the industry’s structure. Also, firms in other markets may be able to perceive opportunities to change industry structure better than existing firms because they have no ties to historical strategies and may be in a position to be more aware of technological changes occurring outside the industry that can be applied to competing in it.”

Competitive Strategy: Techniques for Analyzing Industries and Companies

Chapter 8: Industry Evolution

By Michael E. Porter, 1980

“We believe the future of retail will include both physical and digital customer experiences. Everything we are doing today will enhance our ability to provide everyone in America with the convenience of shopping for anything, anytime, anywhere. We are incredibly excited that it is Kroger who is bringing Ocado technology to the U.S. for the first time.

The platform includes online ordering, automated fulfillment, and home delivery capabilities, so it’s a perfect fit with our vision and strategy. We look forward to innovating together with Ocado to enhance Kroger’s digital and robotics capabilities.”

Rodney McMullen, Chairman & CEO

Kroger Inc.

First Quarter Conference Call

June 21, 2018

For the supermarket industry, Amazon’s purchase of Whole Foods was an existential moment. A new competitor utilizing a non-traditional channel of distribution, the Internet, planned to obsolete the industry, putting all supermarket stores out of business. And with a competitor not required to make a profit, it put a bind on an industry that needed to create profits to enable it to invest in the systems necessary to compete successfully in the future. For Amazon, entry into the supermarket industry became a logical extension of its retail presence. And, as its 2018 sales remain on a path to exceed $240 billion, this entry acted to underpin its future revenue growth, which requires entry into larger and larger industries. Thus, the supermarket industry, which appeared a dinosaur ready for extinction much as the book industry two decades earlier, would support Amazon’s long term goals of transforming all of retail. In fact, if one read the press articles on Amazon’s entry, it sounded as if Amazon stood victorious without a shot being fired with the supermarket industry already dead.

However, the real world continues a messy place, in which both the Internet and physical retail stores co-exist. In fact, for many industries, the consumer needs to see, feel, and experience the items prior to purchase. The supermarket industry is such an industry, especially for fresh produce. In addition, the supermarket industry participants include large retailers with significant financial resources and industry scale to support their long term competitive position in an inherently low margin business. Lastly, delivering food items through the Internet is neither cheap nor necessarily efficient, as moving small packages of goods via truck delivery creates much more expense per item than delivering a large truck packed with pallets of individual goods. In addition, a full trucking cold chain, requiring specialized trucks and equipment to preserve goods from the distribution point to the consumer, must be put in place. These are but a few of the issues in entering a mature, highly competitive industry with multiple players possessing significant scale and resources to counter a new entrant.

The large players in the supermarket industry include companies such as Kroger, Walmart, and Costco. These companies possess sales of $130 billion, $500 billion, and $140 billion, respectively. With Amazon initially entering their sector through the Internet then adding Whole Foods to have a physical presence, each one of these companies responded in a different way. Walmart bought Jet.com in 2016 to provide the IT infrastructure and executive management needed to meet Amazon toe-to-toe on the Internet. In addition, Walmart added robotic picking recently to select stores to automate the online order/in-store pick-up process. Kroger leveraged its internal IT to provide data analytics on over 70 million households that shop there, every bit as detailed as Amazon’s analytics. They added to this with a recent link-up with Ocado, the UK provider of automated picking systems for stores and warehouse systems to automate Internet sales to provide a truly competitive offering to the consumer. Costco, as does Kroger, continues to leverage its vast database on the 50+ million households that shop there. This enables customized offerings to its shoppers. In addition, with the advances in automated picking systems and the integration of online ordering, Costco, as well as other large box retailers, possesses the ability to convert a portion of its large stores to dedicated Internet order fulfillment. And as selling space shrinks over time, it can naturally add this to its online warehouse and fulfillment structure as it establishes this structure in each store. Given these moves to make each of the key players competitive in the industry, Amazon possesses much less of an advantage than when it entered other retail sectors in the economy.

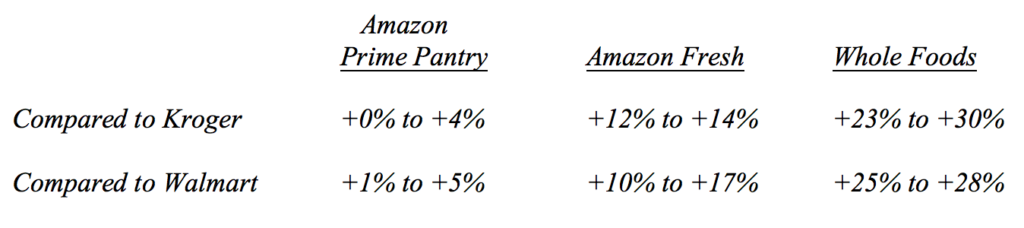

And while the systems, processes, and physical structures provide the ability to go to toe-to-toe with Amazon, the real “Rubber Meets the Road” occurs at the price level, whereby consumers get to see the offerings from each retailer. And while Amazon may have the opportunity to undercut prices in other areas of the economy, that possess large margins and high costs enabling it to grab share, the supermarket industry does not fit this description. In fact, Amazon stands at a competitive disadvantage due to the buying power of the large retailers. When Amazon went to Procter & Gamble and other packaged goods companies to request special packaging and lower prices than the existing players in the industry, Walmart reminded these companies that the company purchased more of their goods than anyone else. In fact, Walmart made it clear that any company that did not give it the lowest unit pricing for its goods stood at risk of losing its business. As Walmart purchases 20% of these companies’ products, such a threat loomed large in their considerations of how to address Amazon’s request, which they politely declined. The following table illustrates a recent pricing study comparing Amazon pricing with that of Kroger and Walmart over the last four months:

As the above Table makes clear, Amazon pricing stands well above Kroger and Walmart for a large portion of its sales and struggles to match them for staples that can ship directly to consumers from a warehouse. Thus, where the “Rubber Meets The Road”, Amazon stands at a competitive disadvantage. And while it may chew up some share from the smaller players in the industry, taking share from the larger companies, such as Walmart, Target, Costco, and Kroger, likely will prove difficult and costly.

With the media viewing every industry as a target for Amazon to roll over, the above statistics make clear that there exists a large gap between perception and reality. And for industries in which the players possess scale, such as the supermarket industry, or in which the existing competitors must possess extremely efficient operations to survive, such as the drug distribution industry, the ability of Amazon to overwhelm the existing entrenched companies, as the press would indicate, stands in question. Furthermore, to enter all of these industries requires, not only technology and organizational capabilities, but significant capital to underwrite the entry costs, put in place the assets, and attract key people with which to wage competitive war. And while Amazon may have shot the first bullets in entering the supermarket industry, the industry appears to have absorbed the initial fusillade, enabling it to gather the troops and weapons necessary for a long bloody struggle. And when the story is written of the history of this war, it may well be titled “The Revenge of the Supermarkets” as they leverage their scale, technology, and capital in a counteroffensive that leaves both sides bloodied, but much of the industry in the hands of the current competitors. (Data from JP Morgan, Credit Suisse, and company reports, coupled with Green Drake Advisors analysis.)

Confidential – Do not copy or distribute. The information herein is being provided in confidence and may not be reproduced or further disseminated without Green Drake Advisors, LLC’s express written permission. This document is for informational purposes only and does not constitute an offer to sell or solicitation of an offer to buy securities or investment services. The information presented above is presented in summary form and is therefore subject to numerous qualifications and further explanation. More complete information regarding the investment products and services described herein may be found in the firm’s Form ADV or by contacting Green Drake Advisors, LLC directly. The information contained in this document is the most recent available to Green Drake Advisors, LLC. However, all of the information herein is subject to change without notice. ©2018 by Green Drake Advisors, LLC. All Rights Reserved. This document is the property of Green Drake Advisors, LLC and may not be disclosed, distributed, or reproduced without the express written permission of Green Drake Advisors, LLC.